Obamacare Too Expensive? Consider This Alternative

Our Exclusive Cost-Benefit Analysis Found Thousands in Savings for the Same Care at the Three Leading Healthcare Sharing Ministries

If you don’t have traditional health insurance sponsored by your employer, you can buy Marketplace coverage under provisions of the Affordable Care Act of 2010—more commonly known as Obamacare. Some 24 million have done that this year. But Obamacare plans can cost policyholders a king’s ransom vs. employer plans: Hundreds of dollars more out-of-pocket in monthly premiums just to get a plan and thousands higher in annual deductibles if you actually use it.

Obamacare policyholders who are eligible for taxpayer-subsidies get an average premium reduction of $705 per year, according to KFF, a health information nonprofit. But they are about to be hit by a bipartisan one-two punch that the American Hospital Association says will make them considerably more expensive: President Joe Biden’s enhanced Obamacare tax subsidies expire at the end of 2025 and President Donald Trump’s newly enacted tax law doesn’t renew them. That and other policy changes are expected to increase premiums for subsidized enrollees.

Luckily, there is an enticing alternative for Christians: So-called healthcare sharing ministries (HSMs) are communities whose members profess their Christian faith, strive to maintain healthy lifestyles, and team up to share payment of each other’s medical bills—and they make seemingly miraculous promises:

· “Save…up to 50 percent on your monthly [healthcare] cost.”

· “Ninety-eight percent satisfaction.”

· “No network restrictions…No fees…The…biblical solution to satisfying your medical costs.”

Hallelujah! But wait! Are these plans legit?

The short answer is Yes, according to Your Consumer Reporter’s assessment of the three largest HSMs—Christian Care Ministry (doing business as Medi-Share), Christian Healthcare Ministries, and Samaritan Ministries. Together, these plans, available in all 50 states, have delivered $23 billion in benefits to their members over the past four decades.

As important, our exclusive cost-benefit analysis shows these ministries can save an example California family $2,350 to $6,550 over one year vs. an equivalent-as-possible unsubsidized Obamacare plan, in dealing with three hypothetical medical care incidents costing a total $21,100.

But the devil is in the details.

For example, HSM membership is contingent on abiding by a Chrisitan lifestyle that includes only engaging in sexual relations within a marriage between one man and one woman. If that’s you, Great! Read on.

However, because 57 percent of Christians say sex between unmarried adults in a committed relationship is “sometimes” or “always” acceptable, according to a Pew Research Center survey, be sure to see our “Faith and Lifestyle Requirements” section below and scrutinize each HSM’s specific guidelines on this, which also cover LGBTQ consumers, use of pornography, alcohol and drug abuse, smoking, and other topics.

If you can’t abide by the faith and lifestyle requirements and join an HSM anyway, you risk important practical consequences: Your membership can be reviewed and cancelled, and your medical bills won’t be shareable.

HSMs’ Costs and Benefits Can Beat Obamacare

While Obamacare plans are insurance, HSMs are not insurance and they don’t cover all the same healthcare problems as health insurance (see below for more detail on the differences). In many ways, the differences make HSMs like a hamburger and Obamacare a four-course meal: You get more on your plate with Obamacare, but it costs more and may be more than you need. Nevertheless, we think it is legitimate to conduct a lunch-to-dinner comparison of insurance vs. not-insurance, because both work to accomplish the same goal—get your medical bills paid according to set rules—and real shoppers can, should, and do compare the two. We’re doing the same thing, but with a more precise methodology, and we’ll give you the tools to do your own comparison.

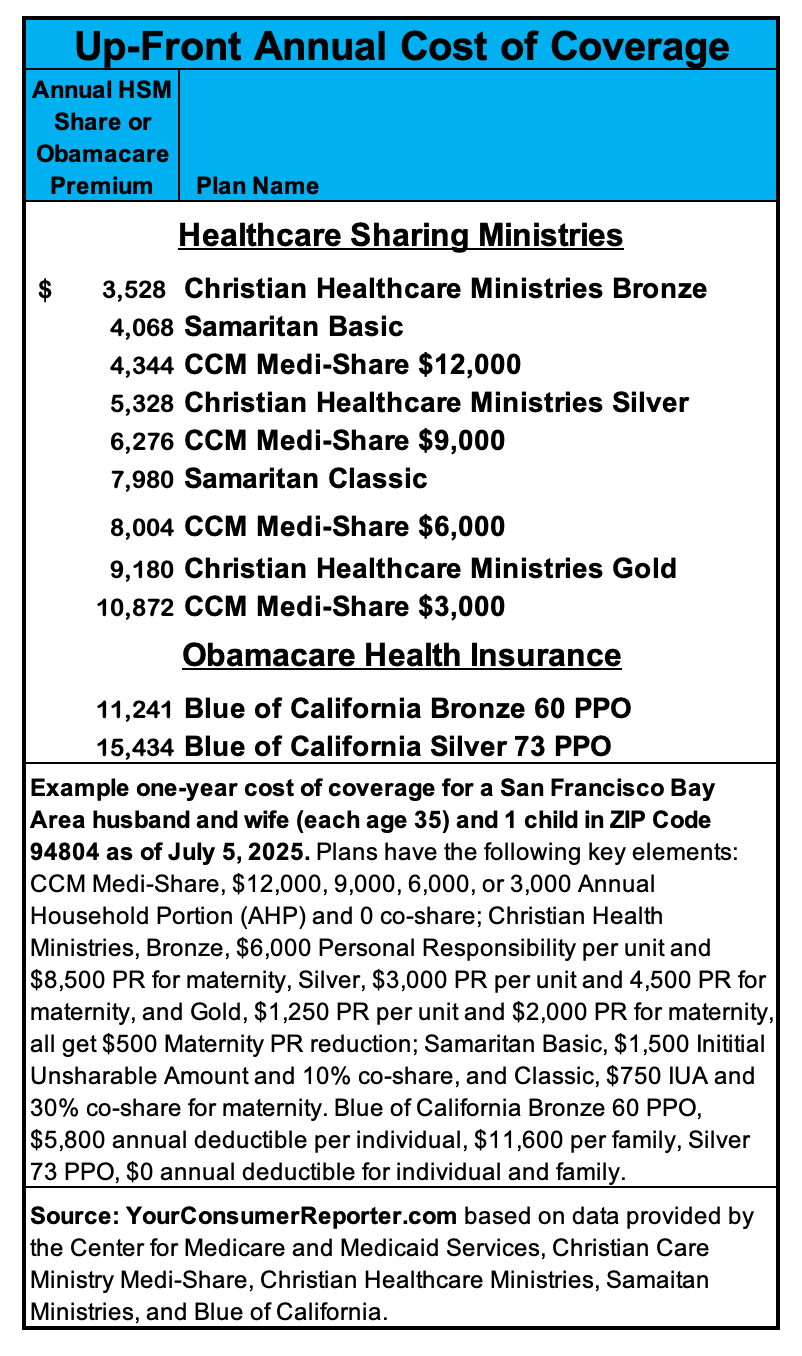

Let’s start with the big driver: Cost. To assess the all-important dollars and cents of HSMs vs. Obamacare, we created an example San Francisco Bay area family with a married husband and wife, both age 35, and one child. Their income is $150,000 a year, which would make them ineligible for Obamacare subsidies. We then obtained current price quotes for the Big Three HSMs’ monthly “share amounts” or “contributions” that our model family would pay, which is the equivalent of health insurance monthly premiums. These amounts are paid to an electronic account or directly to other members with a need, depending on the plan. We also got premium quotes for our family for a California Blue PPO plan that was as similar as possible to the HSM plans, and for a second not-so-similar Blue plan with a desirable zero deductible. We then toted up the monthly costs over a year.

As shown below, almost all the HSM annual share costs for our model family were thousands of dollars lower than the two Obamacare annual plan premiums:

So far, so good. But premiums and shares are only part of the total insurance/HSM cost equation. They’re the price of admission that gets you into the tent; however, because they must be paid every month, providers have a competitive incentive to reduce that highly visible Ouch! and they can do that by shifting more of the total cost of coverage to less-obvious charges—via deductibles, household shares, co-payments and co-shares, and benefit limits—which don’t hit you until you use the coverage. So we applied each plan’s current benefit payment rules to three example medical care incidents.

That’s tough to do, which is why comparing plans is difficult for consumers. Every medical care incident is different, and the number of specific treatment billing items can range from one to 1,000 or more, depending on the complexity of the case. As it turns out, the federal Centers for Medicare and Medicaid Services mandates that Obamacare and other health insurance providers disclose coverage examples showing how much their plans and the policyholder would pay for three example incidents. CMS says this shopping tool can be used by consumers “to compare the portion of costs you might pay under different health plans.”

To put these cost calculations on a level playing field, CMS created standardized treatments for each medical case, right down to the insulin syringes, fiberglass leg cast, and prenatal vitamins. We obtained the underlying data for the specific treatment items, billing codes, and itemized prices based on an estimated national average for each case—from physician services, pharmaceuticals, and imaging to medical supplies, emergency room fees, and lab work. The three cases, which CMS labels as “Peg is having a baby,” “managing Joe’s Type 2 diabetes,” and “Mia’s simple fracture”—together involved 165 individual charges totaling $21,088 in cost and provided a robust example of the medical needs a family might realistically have over a year—not catastrophic, but also not minor.

We then applied each HSM plan’s rules to these treatment costs to estimate how each HSM plan would provide benefits to our example family over a year. The results allowed us to calculate and compare the total and net costs and benefits of the HSMs head-to-head with each other and with the Obamacare plans to reveal which provided the best to worst deal. We sent our calculations to Medi-Share and Samaritan and reached out to CHM, but all three declined to confirm, correct, or respond.

How The Plans Compared

This is what each plan cost our example family for the same health care:

If our example family had no insurance or HSM, it would have to pay $21,088 in medical bills for the three incidents in our model. By joining Samaritan Classic and making $7,980 in annual share payments plus $10,211 in out-of-pocket costs to providers—whose costs are not eligible for sharing under plan rules—the family pays a total of $18,191 for $21,088 in medical services. Our example family thus obtained a net benefit of $2,897.

Christian Healthcare Ministries’ Silver plan provided a similar net benefit. But note that the up-front annual contribution payments were lower, while the non-eligible costs ran higher. That’s one way providers can lower the visible fixed prices, while making up that savings by raising the less-appreciated variable costs. If you and your family are generally healthy, the sure thing of lower HSM share costs are a better deal for you, because you might incur little or no variable costs in a given year. Unfortunately, no one knows for sure what his health care needs will be in the coming year, which is why insurance and HSMs were created.